| Home | About | Archives | RSS Feed |

The Independent Investor: General Motors — Back to the Future

|

|

It will be the largest public offering in U.S. history. A total of $23.1 billion was raised, including $4.35 billion in preferred stock. That was no small accomplishment, given the recent sell-off in world markets. General Motors is back.

It will be the largest public offering in U.S. history. A total of $23.1 billion was raised, including $4.35 billion in preferred stock. That was no small accomplishment, given the recent sell-off in world markets. General Motors is back.

What a difference two years make. Over that time, I had written several columns at first advocating letting GM go bankrupt (which it ultimately did). It was either that or a merger, if they could find an auto company that was willing to step up to the plate and buy it. There were no takers. When the government announced its last resort of a $49.5 billion bail out last year, I had mixed feelings.

After the huge bank bailouts, I wasn't happy about rescuing GM. I believed that the auto company deserved its fate. Its management had guided the company downhill ever since the mid-90s with the help of the labor unions. It was their arrogant "we know best" attitude in the face of obvious changes in the global automotive marketplace (such as the move toward smaller, more fuel-efficient cars) that really bothered me.

On the other hand, I also knew that we didn't need another avalanche of layoffs in the face of an unemployment rate that was climbing at 400,000 lost jobs per month. And GM employees were only the tip of the iceberg when it came to lost jobs. The ripple effect on auto suppliers would have to be added to the GM jobs. Then there were the dealerships across the nation. Car dealers provide enormous benefits to just about every local community in America in the form of jobs, taxes and charitable giving, while providing increased shopping traffic to the community they reside in.

By the time I took account of the enormous blowback GM and Chrysler's demise would cause, I reluctantly agreed that the bailout was better than the alternative although my stance was not very popular among readers.

In September 2009, in "Why Americans Should Become Detroit's Long-Term Investors," I wrote the following about the billions in taxpayer money we were investing:

Now, as we like to say in the money-management business, the past is no guarantee of future performance, yet there is a chance if we have a little patience here we too could walk away with a big return. Besides, what do we the taxpayers have to lose? Sure, I know there will be some that say the government has no business becoming the major shareholder in American auto companies and should exit this investment at the earliest possible time. Some will even say it is un-American if we don't. I say it's a little too late for those attitudes. The horse is already out of the barn. So go ahead and call me a socialist. I say we took a huge risk when no one else would, and we deserve a commensurate return on this investment. Now, as we like to say in the money-management business, the past is no guarantee of future performance, yet there is a chance if we have a little patience here we too could walk away with a big return. Besides, what do we the taxpayers have to lose? Sure, I know there will be some that say the government has no business becoming the major shareholder in American auto companies and should exit this investment at the earliest possible time. Some will even say it is un-American if we don't. I say it's a little too late for those attitudes. The horse is already out of the barn. So go ahead and call me a socialist. I say we took a huge risk when no one else would, and we deserve a commensurate return on this investment.Now that presumes I have some faith in the future of the American auto industry, and I do. All I have read concerning the on-going restructuring taking place in research and development, in manufacturing processes, and management structures indicate to me that the Big Three are getting their act together. Ford is clearly on the right path and so are GM and Chrysler. After all, none of them have lost their main competitive edge—American labor and ingenuity. I'll bet on that. So let's hang in there. I believe a little patience will pay off for all of us down the road.  |

So far GM has returned $9.5 billion of that loan. With this offering, another $13 billion will flow back to the government, leaving taxpayer ownership at roughly 26 percent, down from 61 percent. It is a shame that the government does not have the patience to hold on to its shares because, over time, I think taxpayers could have made a substantial profit.

I guess removing the "government motors" stigma from the company outweighed the profit motive. Over the next few years, the government will continue to sell down its position in the same manner that they are now reducing their ownership of Citibank (at a profit). It looks like most of our investment will be recouped and at a far faster than I imagined.

Bill Schmick is an independent investor with Berkshire Money Management. (See "About" for more information.) None of the information presented in any of these articles is intended to be and should not be construed as an endorsement of BMM or a solicitation to become a client of BMM. The reader should not assume that any strategies, or specific investments discussed are employed, bought, sold or held by BMM. Direct your inquiries to Bill at 1-888-232-6072 (toll free) or e-mail him at wschmick@fairpoint.net. Visit www.afewdollarsmore.com for more of Bill's insights.

| Tags: GM, bailout |

@theMarket: Corrections Are Good for the Soul

It was long overdue. For weeks, the stock market has registered overbought conditions and still it forged ahead. Investors had driven the averages back to yearly highs and only then did the rally run out of steam. Now it's time to step aside and watch.

It was long overdue. For weeks, the stock market has registered overbought conditions and still it forged ahead. Investors had driven the averages back to yearly highs and only then did the rally run out of steam. Now it's time to step aside and watch.

"Is this the start of something big or should I just stay put?" asked a retired client from Pittsfield who has recouped much of his 2008 loses over the last year.

"Stay put," I said, "because this pullback will be short and unless you are a day trader, too volatile to do more than add to existing positions."

I'm thinking we could see the stock markets drop as much as 5 percent, which from here isn't such a big deal. Take the S&P 500 Index, for example. This week it hit an intraday high of 1,227 (almost 10 points higher than its peak in April). A 5 percent decline from that level would put the average at 1,165, a mere 30 points down from here. That's not worth getting excited about.

As a rule of thumb, I believe that 5 percent to 10 percent corrections in the stock market are the "price of doing business" or the risk one must accept in equity investing. These kinds of corrections occur 2-3 times a year on average. And it is not just equities that are falling.

Commodities are also declining. As I look at the present spot price of gold, the precious metal is off over $40 an ounce while silver is down $1.50 an ounce and oil has plummeted over $3 a barrel — in just one day. Commodities tend to have extremely sharp, if short, corrections that tend to wilt most amateur investors' resolve to stay invested. It appears that once again those who have chased energy, precious metals and agricultural commodities are suffering big reversals this week. Rather than buy this weakness, they tend to sell in panic.

For those with bullish convictions, this pullback is a buying opportunity, not only in commodities but stocks in general. This coming week should provide further opportunities to establish new positions. Some of the areas I favor for additional investment are emerging markets, real estate such as REITs, commodities, commodity companies and selected technology.

As for the culprits that triggered the pullback, most of the negative events have something to do with governments. The on-again-off-again saga of the European debt crisis has reignited fresh worries over Ireland's struggle to rescue its financial system. It has led investors to re-examine Europe's financial situation in general.

At the same time, China is rumored to be hiking interest rates in an attempt to slow their economy. That would spell bad news for everyone since China has become the new locomotive of global growth. Over in Korea, where the G20 adjourned without agreeing on how to curb the growing currency war, left investors worried and disappointed over the fate of the U.S. dollar.

All of the above are serious issues but they have been with us throughout the year. China has raised rates before and emerging market growth is still quite healthy. The problems of Europe's smaller economies will continue to plague the Euro and the European Community for the next few years, but has not stopped their stock markets from enjoying substantial gains over the last six months.

The financial world is fully aware of every nuance of the currency debate. The dollar has declined since late August, sending stocks and commodities ever upward. None of this is new. Consider this pullback a healthy correction and that's all you need to know.

All these reasons for the sell-off will still be with us a month from now when the averages have regained their upward ascent, so don't put too much stock in today's headlines. They are fleeting at best. Focus instead on the opportunities this sell-off will present.

Bill Schmick is an independent investor with Berkshire Money Management. (See "About" for more information.) None of the information presented in any of these articles is intended to be and should not be construed as an endorsement of BMM or a solicitation to become a client of BMM. The reader should not assume that any strategies, or specific investments discussed are employed, bought, sold or held by BMM. Direct your inquiries to Bill at 1-888-232-6072 (toll free) or e-mail him at wschmick@fairpoint.net. Visit www.afewdollarsmore.com for more of Bill's insights.

| Tags: corrections, stocks, metals, China, commodities |

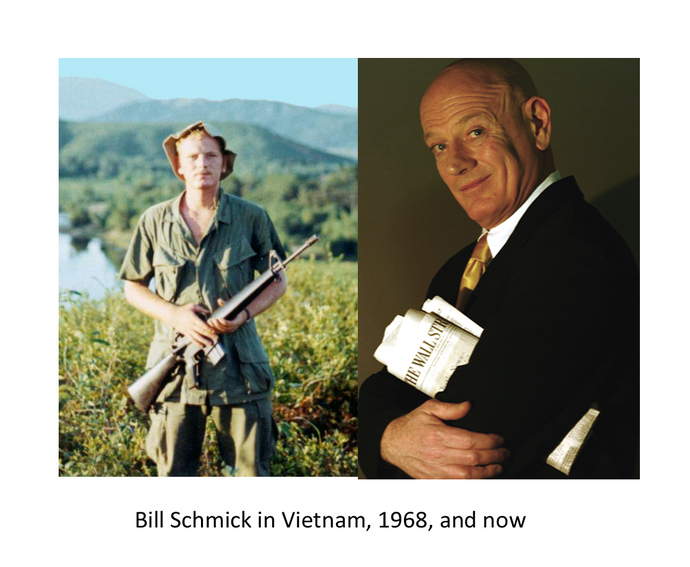

Veteran Takes Deserved Day Off

|

Yes, that really is our finanical columnist Bill Schmick in Vietnam 42 years ago. Bill, who served four years as a Marine, took Veterans Day off. Thanks, Bill, to you and all veterans.

| Tags: veterans |

The Independent Investor: Sour Grapes

As the G20 conference gets under way today in Korea, I expect the currency war will escalate now that the U.S. Federal Reserve has launched the second round of quantitative easing. As the dollar continues to decline, our trading partners are getting back a little of their own and they don't like it.

As the G20 conference gets under way today in Korea, I expect the currency war will escalate now that the U.S. Federal Reserve has launched the second round of quantitative easing. As the dollar continues to decline, our trading partners are getting back a little of their own and they don't like it.

Over the last week or so, the Fed's QE II announcement has been greeted by a chorus of howls from all over the world. Germany's finance minister called U.S. policies "clueless" while Chinese officials quickly added their own criticism.

"As long as the world exercises no restraint in issuing global currencies such as the dollar, then the occurrence of another crisis is inevitable," stated Xia Bin, an adviser to China's central bank.

Brazil's finance minster, Guido Mantega, went further when he said, "Everybody wants the U.S. economy to recover, but it does no good at all to just throw dollars from a helicopter."

Those are just a few choice criticisms but there were many more from nations throughout the world accusing the U.S. of everything from currency manipulation to exporting inflation. They may be right but that doesn't mean we are wrong.

For decades, the U.S. has been running a major trade deficit with our international trading partners. All these countries that are squawking about QE II have been major beneficiaries of a monumental trading imbalance with the U.S. both now and in the past. In Latin America, for example, Brazil, among others, has benefited mightily by keeping its own currency artificially low and exporting huge quantities to the U.S. China is another master of currency manipulation and has followed a weak currency/high export policy for years. Germany is also enjoying booming exports, trade surpluses, low debt and an unemployment is expected to fall to 1990s levels thanks to a weak euro.

So after carrying the weight of the rest of the world's exports for years, the U.S. is fighting back and well it should. It is our nation and not any of the above countries, which is suffering a high unemployment rate, a slow growth recovery, huge trade deficits and a record debt load. We are simply following the same prescription both Japan and Europe followed after WWII, which Latin America followed after their Lost Decade of the 1980s. China's economic miracle is founded and continues to grow along these same economic principles.

Now that America has decided to play the same game, cries of "foul" echo across the world. It is true that America's actions will cause problems for economies around the world. Right now it makes a lot of economic sense for foreigners to borrow in dollars where interest rates are at rock bottom and then invest that money in building plants and equipment back home where interest rates and local currencies are higher. Of course, their governments already hold huge dollar reserves in the form of U.S. Treasury bonds. Foreign central banks fear that all this additional dollar borrowing may cause inflation in their own countries.

You might ask how critics can take the moral high ground and point a finger when for years they have been doing the same thing to us and acting as if America was their own private export market. Nations, however, are not individuals; which brings to mind a quote of Thomas Jefferson, one of our founding fathers:

"Money, not morality, is the principle commerce of civilized nations."

Bill Schmick is an independent investor with Berkshire Money Management. (See "About" for more information.) None of the information presented in any of these articles is intended to be and should not be construed as an endorsement of BMM or a solicitation to become a client of BMM. The reader should not assume that any strategies, or specific investments discussed are employed, bought, sold or held by BMM. Direct your inquiries to Bill at 1-888-232-6072 (toll free) or e-mail him at wschmick@fairpoint.net. Visit www.afewdollarsmore.com for more of Bill's insights.

| Tags: currency, trade, deficit, G20 |

@theMarket: Markets Are Going Higher

|

Fed Chairman Ben Bernanke's putting his faith in the market. |

The above headline may be a bold statement, especially when the averages are already at levels that surpass this year's stock-market highs. But the actions and words of the Federal Reserve Bank this week convinces me that stocks have substantial upside ahead of them.

As I predicted, this week was a big one for investors and the country. The mid-term election results and the resulting legislative gridlock in Washington most pundits expect leaves the Fed as our only hope in reviving the economy and reducing unemployment. (see yesterday's column "Don't Fight the Fed.")

The $600 billion in additional quantitative easing (QE II) and Chairman Ben Bernanke's Op-Ed piece in the Washington Post makes obvious that not only is the Fed targeting stronger growth in the economy but also higher prices in the stock market.

It is the first time in my career that a Fed chairman has explicitly targeted stocks as a tool to increase consumer spending, grow the economy and reduce unemployment.

Imagine my surprise when a day later, the central bank of Japan stated the very same thing but went a step further by also targeting real estate prices in its country.

This takes government support of the economy to an entirely new level in my opinion. During the financial crisis and its aftermath, the government (the Fed, U.S. Treasury and both the Bush and Obama administrations) has on several occasions provided a back stop to the markets. They took actions to save corporations, provided support for declining securities such as mortgage-backed securities, even money markets, and promised to support or bail out the U.S. financial markets with all the power at their disposal. It was one of the main reasons back in early 2009 that I turned bullish on the stock markets. I was betting on the government because they have much deeper pockets then the private sector and if they failed to fulfill their promise we were all doomed anyway.

This week's comments from Bernanke have taken that implicit promise of "support" a big step further. If I read this right, Bernanke is saying that consumers and corporations are still worried about the economy and their own finances. Higher stocks, according to Bernanke, will restore confidence as Americans see their savings rebound. That confidence could lead to additional spending, which would mean more growth in the economy and ultimately lower unemployment. Therefore, insuring that stock prices go higher would accomplish the Fed's mandate of lower unemployment.

Now that does not mean the Fed is simply going to jack up the market in one big melt-up. There will still be corrections. The market is overdue for one right now but over the longer term, at least the next few quarters, I think the fix is in. So if you have been sitting in Treasury bonds or cash waiting for the inevitable second collapse in stocks you may have to wait several more years. In the meantime, you could miss out on a substantial rally in equities.

I also think that we will finally see a dip in the unemployment rate over the next few months. The stimulus money that was spent during the run-up to the elections has generated additional jobs and those jobs are beginning to show up in the data. In addition, I expect U.S. productivity will begin to falter as the economy perks up. So from where I sit, the next few quarters look pretty good for the stock market.

Bill Schmick is an independent investor with Berkshire Money Management. (See "About" for more information.) None of the information presented in any of these articles is intended to be and should not be construed as an endorsement of BMM or a solicitation to become a client of BMM. The reader should not assume that any strategies, or specific investments discussed are employed, bought, sold or held by BMM. Direct your inquiries to Bill at 1-888-232-6072 (toll free) or e-mail him at wschmick@fairpoint.net. Visit www.afewdollarsmore.com for more of Bill's insights.

| Tags: Bernanke, Federal Reserve, stock market |